- Big tech firms are seeing early AI-driven cloud revenue growth, but concerns around declining cloud-margins and negative free cash flow persist

- AI is less successful in customer-facing tasks but more adept at cutting costs in back-office tasks benefitting banks; Advertising, gaming, and e-commerce are key sectors to benefit

- We prefer players with AI adoption benefits in their core businesses, exposed to leading LLMs and with a lower reliance on expensive Nvidia chips

Related insights

Rising hyperscalers capex signals success of AI pilots. After years of heavy AI capex, US hyperscalers are delivering robust growth in their cloud revenue, either meeting or exceeding street expectations. However, cloud margins faced pressure due to rising depreciation and amortisation costs, while cash flow concerns deepened as 3Q25 guidance points to higher AI capex for 2025 and 2026. We think the market is overly focused on lower cloud margins and overlooking the benefits of AI adoption in their core businesses, such as advertising, gaming, and e-commerce. For example, Meta, Alibaba, and Tencent benefit from higher click-through rates in their advertising business, while Amazon benefits from more personalised recommendations plus a reduction in fulfilment costs supported by AI-led Robotics.

While AI is less successful in customer-facing tasks as they involve unstructured interactions and human emotions, it is more adept at repetitive, data-intensive back-office tasks. Banks are also likely to benefit from lower costs for compliance and documentation. We expect the free cash flow of hyperscalers to only stabilise in 2027, mainly driven by higher AI revenue. With AI deployment (Inferencing) likely to overtake AI training by the end of 2025, revenue could see a big jump in 2027.

Cloud revenue accelerates, margin trends mixed. Latest results showed that overall operating margins rose for some players despite a decline in cloud margins. Annual cloud revenue growth accelerated across major hyperscalers. Amazon’s cloud revenue accelerated from 17.5% in Jun 2025 to 20.2% in Sep 2025, Microsoft from 25.6% to 28.2%, and Alphabet from 31.7% to 33.5%. Alibaba’s cloud revenue growth is also expected to accelerate from 25.8% in June quarter to 28.1% in September quarter. Conversely, cloud operating margins softened across most peers, except for Alphabet (17.1% in Sep 2024 to 23.7% in Sep 2025) and Alibaba (guided stable at 8.8%).

Overall operating margin trend was mixed. Meta’s operating margin dropped from 42.7% in Sep 2024 to 40.1% in Sep 2025, while Alibaba’s EBITA margin is expected to drop from 17.2% to 5.0% (during the same period), due to intensified quick commerce competition. On the other hand, Microsoft (46.6% to 48.9%) Alphabet (32.3% to 33.9%), Amazon (11.0% to 12.1%) delivered expansion. We also expect Tencent’s operating margin to expand from 36.6% to 38.1% during the same period.

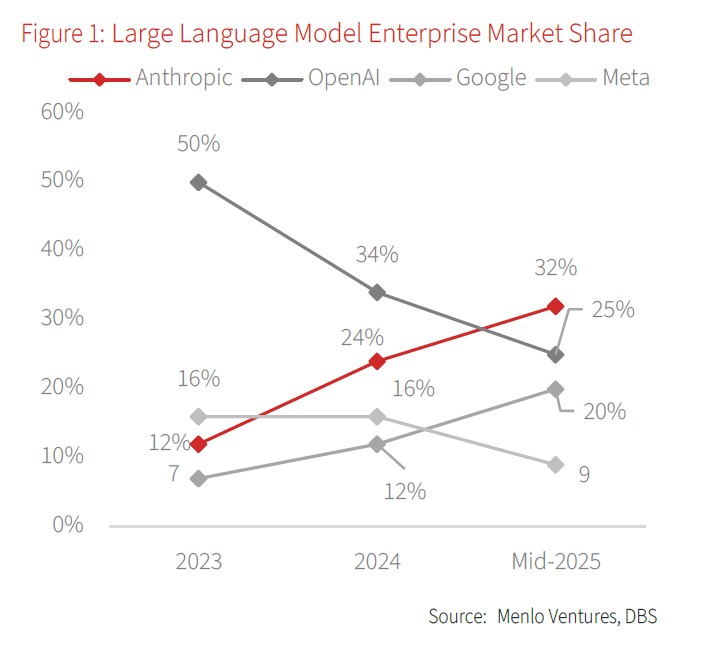

AI themes at the forefront. According to Menlo Ventures, Anthropic has emerged as the leading enterprise Large Language Model (LLM) provider with 32% market share in mid-2025. OpenAI’s share has dropped to 25%, from 50% in 2023, while Alphabet’s Gemini has reached 20% market share after being a late starter. Alphabet is leveraging its decade-old investment in its custom AI chips, Tensor Processing Units (TPUs) to efficiently handle AI Training & inference workloads at a fraction of cost than Nvidia chips. Anthropic is deploying Amazon’s Trainium Chips for training its models and is readily accessible to AWS customers via Amazon Bedrock. Alibaba also offers its own innovations: its popular Qwen models in China, and its own Parallel Processing Unit (PPU) for AI inferencing in the long term.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.