Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

A repeat of 2008 GFC contagion on the cards? Not likely. After the publication of our CIO Perspectives: US Commercial Real Estate – The Next Shoe to Fall (dated 25 April 2023), the questions one would naturally ask are:

- What if the shoe indeed falls and what are the economic implications?

- Will this be a repeat of 2008’s Great Financial Crisis (GFC)?

- What is the impact on global risk assets?

These are valid questions. With the challenges of a slowing economy, persistent inflation, and elevated bond yields, it is only right for portfolio allocators to tackle these issues head-on and prepare for potential economic/financial ramifications should the US commercial real estate (CRE) space implode.

Question 1: What if the shoe indeed falls and what are the economic implications?

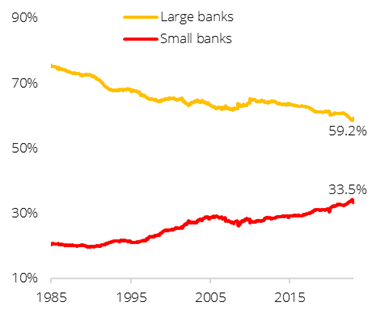

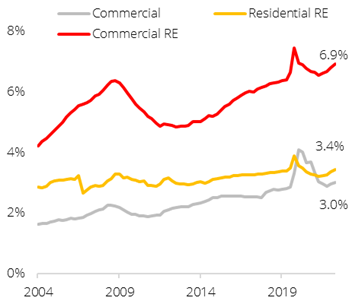

- US regional banks will be the hardest hit should the CRE space implode. To determine the potential impact, we look at how exposed the US economy is to this segment.

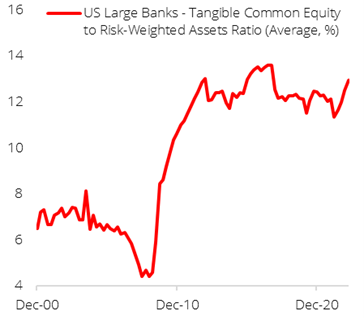

- A widely used gauge for banks’ financial health is the tangible common equity to risk-weighted assets (TCE/RWA) ratio. In the run-up to the GFC of 2008, the TCE/RWA ratio for US large banks (proxied by JPMorgan Chase, Citigroup, and Bank of America) deteriorated from 6.3% in Dec-2006 to 4.4% by Jun-2008 (right before the crisis).

- Banks operating on low TCE/RWA ratios run the risk of having their shareholders’ equity wiped out should liabilities spike, leading to insolvency. But post-GFC, banks’ equity position underwent a sea change. Average TCE/RWA ratio has improved markedly to 13.0% (as of Mar-2023), putting these banks in a better position to weather future shocks.

- Besides, US large banks no longer have the same outsized exposure to CRE and henceforth, they can continue to provide liquidity and funding to the economy should the former implode.

Question 2: Will this be a repeat of 2008’s Great Financial Crisis (GFC)?

- Comparing the situation today with 2008, we believe that the probability of a GFC redux is low given that banks today are much better capitalised.

- A widely used gauge for banks’ financial health is the tangible common equity to risk-weighted assets (TCE/RWA) ratio. In the run-up to the GFC of 2008, the TCE/RWA ratio for US large banks (proxied by JPMorgan Chase, Citigroup, and Bank of America) deteriorated from 6.3% in Dec-2006 to 4.4% by Jun-2008 (right before the crisis).

- Banks operating on low TCE/RWA ratios run the risk of having their shareholders’ equity wiped out should liabilities spike, leading to insolvency. But post-GFC, banks’ equity position underwent a sea change. Average TCE/RWA ratio has improved markedly to 13.0% (as of Mar-2023), putting these banks in a better position to weather future shocks.

- Besides, US large banks no longer have the same outsized exposure to CRE and henceforth, they can continue to provide liquidity and funding to the economy should the former implode.

Question 3: What is the impact on global risk assets?

- The impact on equities, credit, rates, FX, and private assets are listed in the table on the following page:

Equities

Risk Areas

- US Financials sector to face significant selling pressure as investors price in potential contagion risks; Small banks with huge exposure to CRE most impacted. Negative sentiments on US financials to spread to other financials plays in Europe and Asia.

- US CRE plays, in particular those with heavy exposure to lower tier offices, will face acute selling pressure (vis-à-vis those with more exposure to the multifamily segment).

- A collapse of the CRE space could translate to job losses and negatively impact domestic consumption.

Beneficiaries

- In Financials, the classic flight-to-quality will ensue with large banks outperforming regional banks. This is in-line with our strategy of going for quality plays in the current environment.

- Rising stresses in the Real Estate and Financials space will raise expectations of policy rate cuts which will be a tailwind for US Big Tech. A lower cost of capital is positive for Tech sector valuation.

Credit & Rates

Risk Areas

- Broader spread widening under tightening lending conditions in the US will hinder access to funding.

- Commercial Mortgage-backed Securities would undergo the most distress, especially the more subordinate tranches of debt, given direct exposure to the CRE sector.

- Bank AT1s would face further contagion-related stress due to expectations of higher NPLs and provisioning eroding equity capital when sentiment is already fragile. AT1s of large banks with the strongest balance sheets are likely to remain firm, although they would not be immune to spill over sentiment in the short term.

- High Yield spreads are likely to widen more significantly given (a) already tighter than average spreads, and (b) tighter funding environment likely impacting the more leveraged companies to a greater extent.

Beneficiaries

- Short-term US Treasuries could gain as yields fall on expectations of policy rate cuts.

- High quality Investment Grade (IG) credit is expected to remain stable given better debt-serviceability, although the Financials and Real Estate sectors could see more significant spread widening. Our base case expectation is that US CRE distress would not lead to a systemic credit crunch, but even if so, the Fed’s extraordinary policies of purchasing IG credit in the Covid crisis shows that they have the tools to prevent such a scenario from escalating.

FX

Risk Areas

- The USD’s trajectory will depend on the extent of the implosion, and the strength of the resultant policy action. Should we see decisive Fed action, the large policy easing should weaken USD against G-10 low-yielders like the EUR and CHF.

- If the Fed falls short, expect an overarching risk-off environment to trigger the USD’s safe haven characteristics. The flight-to-safety dynamic is likely to benefit the USD.

Beneficiaries

- Should the shock evolve into a global contagion, the USD is likely to be the outperformer within the G-10 space. Regardless, the traditional safe havens like the JPY and CHF should also be supported.

Private Assets

Risk Areas

- Potential failures in regional bank sector could exacerbate the challenging capital raising environment for private assets, as lenders and capital providers price in greater risk.

- Private asset structures involving high use of leverage impacted by credit tightening.

- Early stage/VC-backed companies may be hit by reduced access to capital. We note first-time fund managers have faced greatest challenges raising capital, while LPs prefer the safety of established sponsors.

- Concern warranted in the riskiest opportunistic/value-added strategies in private real estate investing, considering challenges in managing vacancies and exposure to refinancing risks.

Beneficiaries

- Tighter bank lending standards could provide a gap for non-bank lenders such as private debt funds to deploy dry powder, as was the case during the GFC. While not immune to heightened risks, direct lending funds may avail credit to going concern companies, at higher lending rates and with stringent protective provisions to address default risks.

- Opportunistic special situations and distressed debt strategies could be poised to benefit as restructuring and defaults rise in a slowing growth environment.

Figure 1: Small banks as % of total bank credit is on the rise

Source: Bloomberg, St Louis Fed, DBS

Figure 2: US Small Bank Loans to CRE as % of GDP

Source: Bloomberg, St Louis Fed, DBS

Figure 3: Improving financial health of US large banks

Source: Bloomberg, St Louis Fed, DBS

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024

Related insights

- Short AUD-CHF on Geopolitical Concerns19 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- AIA Group19 Apr 2024