- Trump threatened additional 100% tariffs on China exports in response to China’s move to tighten export controls of rare earths and critical minerals

- Additional US tariffs and export controls (including those critical software) are set to begin from November 1

- Markets reacted negatively, with both the S&P 500 and NASDAQ falling 2.7% and 3.6% respectively

- We remain constructive on technology despite pullback; secular growth prospects continue to be buoyed by AI adoption and ecosystems

- Pragmatism to prevail over time; latest market correction offers an opportunity for investors to enter the market at more favourable valuations

Related insights

Trade tensions, here we go again. In an unexpected turn of events, the US has threatened to impose additional tariffs of up to 100% in retaliation to China’s decision to tighten export controls on rare earths and other critical materials. The US is also reportedly implementing new export controls on a broad range of products – including software for semiconductor designs – as early as 1 Nov 2025. While this sudden escalation has reignited trade tensions between the world’s two largest economies, we view the latest developments as short-term headwinds rather than indications of structural deterioration in the broader trade framework. As such, we maintain our constructive views on global technology, AI-led themes, and Asia ex-Japan equities.

AI ecosystems primed to accelerate. The latest market rout has undoubtedly impacted global technology-related names. The NASDAQ composite, for example, fell 3.6% on the Friday that China announced its rare earths export controls. However, we remain sanguine on the prospects of technology given the strong secular trend of continued AI adoption. In particular, we are constructive on the “sovereign AI” trend. This refers to how governments across the globe are expediting their deployment of AI to strengthen self-sufficiency by focusing on leading-edge technology, semiconductor capacity, AI infrastructure, cloud networks, application innovation, cybersecurity, and uninterrupted power generation.

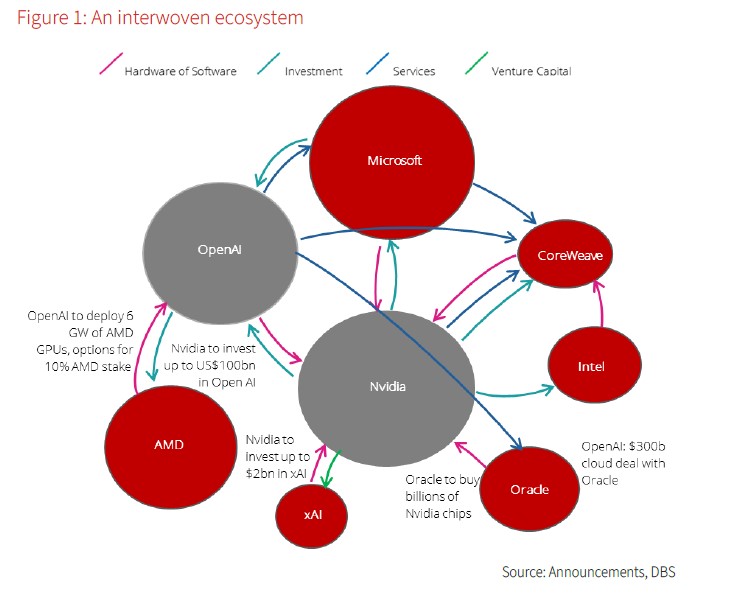

The self-reinforcing capital ecosystem, a model increasingly prevalent among US hyperscalers and technology leaders, represents a potential template that governments may actively encourage to expedite the critical infrastructure buildout process.

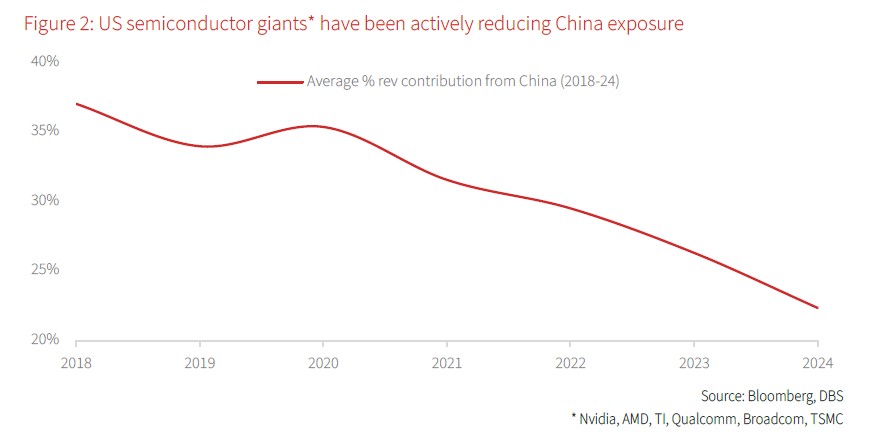

Technology firms are diversifying their revenue. Indeed, leading semiconductor supply chain entities have been actively diversifying their operations and revenue mix, a trend significantly motivated by the US’ progressively stringent export restrictions. Our tracking of six prominent semiconductor and IC design companies reveals a substantial reduction in revenue derived from the Chinese market, plummeting from nearly 40% in 2018 to approximately 22% in 2024. This strategic realignment, whether voluntarily initiated or compelled by external pressures, has consequently diminished these industry leaders' reliance on a single market. Should the Trump Administration’s threats of intensified export controls or outright bans against China materialise, their impact on the growth and fundamental stability of these now considerably more diversified companies is anticipated to be manageable.

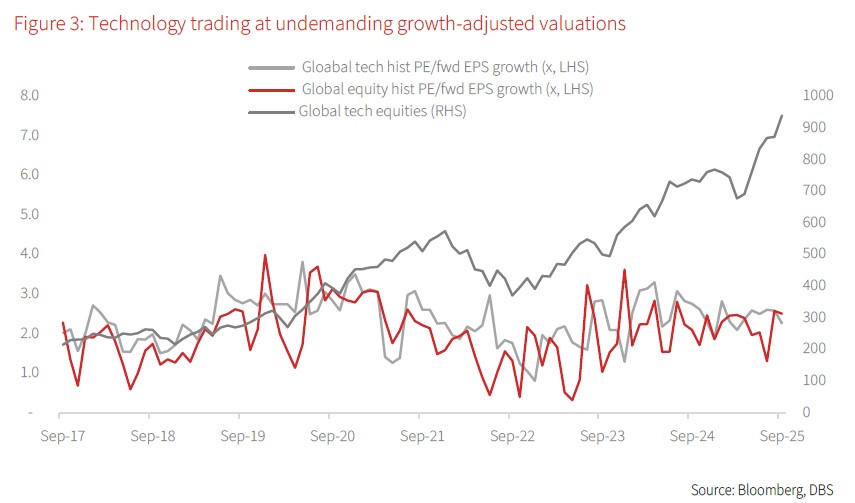

Not-so-premium valuations. While sceptics often cite premium valuations as a reason to remain cautious in the technology sector, we argue that such concerns overlook a more relevant measure: growth-adjusted valuation. On a forward price-to-earnings growth (PE/G) basis, the sector appears far from expensive. Despite delivering exceptional returns since 2017, global technology currently trades at a forward PE/G of 2.3x — not only at par with its long-term average, but also broadly in line with, if not cheaper than, the broader global equity markets.

This underscores a critical point: the sector’s outperformance has been largely earnings-driven, less on multiple expansion. In other words, strong investment returns have been underpinned by robust fundamentals. Structural developments continue to support this earnings trajectory. Secular themes such as AI adoption, cloud migration, digital transformation, and automation remain in the early innings, providing long-term visibility on revenue and margin expansion across key subsectors.

Technology – still the secular growth darling. The global chip market alone is projected to approach USD1tn by the end of the decade, underpinned by sustained demand for computing power and intelligent automation. Meanwhile, global technology spending is on track to exceed USD5tn by 2025, surpassing the size of the German economy. We see recent volatility as transitory, with structural tailwinds from AI adoption and digital disruption continuing to anchor a long-term constructive outlook for the technology industry across IC design, software applications, platform ecosystems, cloud computing, cyber security, and the broader semiconductor value chain. This will be supported by massive capital allocations and strong commitments by key stakeholders to ensure the success of the sector moving forward.

M&A to provide an additional boost. From AMD acquiring Xilinx, Broadcom acquiring VMWare, to Palo Alto + Cyber Ark, and the recent deal on Softbank proposing to acquire part of ABB’s automation business; the M&A environment will remain dynamic among the leading industry players as they aim to strengthen their ecosystems, market penetration, and breadth of innovation. This will be an additional boost to the sentiment and support the broader technology sector’s outlook.

Reason will prevail. The on-and-off trade détente and strains are not something new to the markets as investors have seen this movie play out repeatedly since 2018. Clearly, both sides have things that they want from each other, suggesting their obvious intention of achieving a pragmatic outcome at the negotiation table.

The market has largely discounted the prevailing uncertainty since the reciprocal tariffs framework was first introduced in April this year. Nonetheless investors remain cautiously optimistic as reflected in recent market run-ups. This correction presents a favourable opportunity for investors to play catch up on or average down their positions in Bigtech and names that will clearly benefit from this enduring secular trend.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.