- Labour market weakness in the US has revived rate cuts as a catalyst for gold, with futures markets predicting a total of three cuts this year

- Fears of “fiscal dominance” to exacerbate de-dollarisation and monetary debasement risks, adding to gold’s appeal

- Geopolitical and macroeconomic uncertainty continues to drive investment demand for gold (both physical and ETF)

- Record gold prices has slowed central bank buying in 2Q25 but buying intention remains strong as fluid geopolitics encourage continued reserve diversification

- Raise 1H26TP from USD4,000/oz. to USD4,450/oz

Related insights

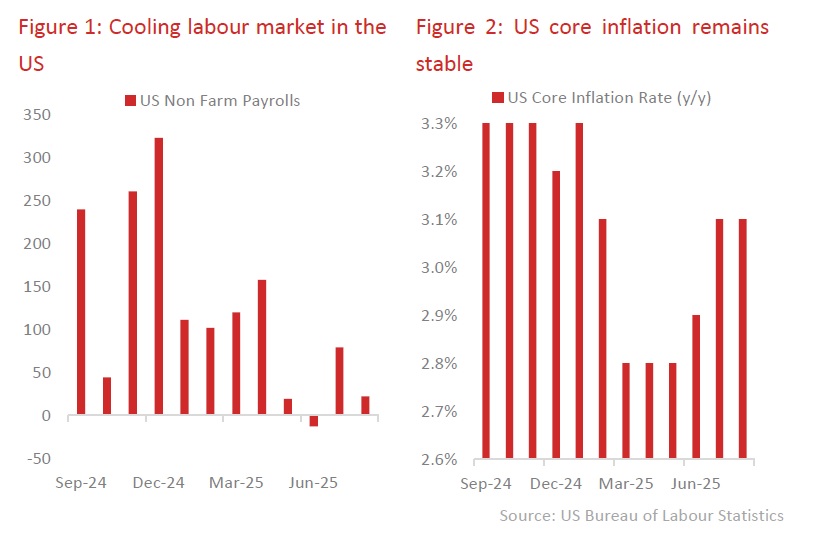

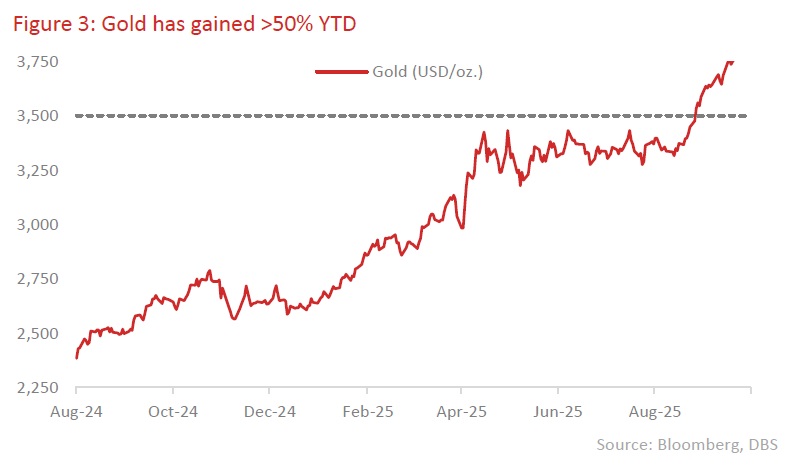

Rate cut catalysts back on the table. Signs of labour market weakness and stable inflation in the US saw the Fed implement a much anticipated 25 bps rate cut in September. A 22k reading for August non-farm payrolls confirmed that lacklustre readings in prior months were not abnormalities while core inflation stabilising at 3.1% for two consecutive months gave the Fed confidence to deliver its first quarter point rate cut this year. This development saw gold breaking out convincingly of its USD3,500/oz. range to reach a new record high of USD3,858 at the end of September. At the time of writing (7 Oct), gold is trading at USD3,960/oz. and looks set for further gains. Undoubtedly, the anticipation for further rate cuts by the Federal Reserve, among other factors, is driving this rally. Currently, Fed funds futures are pricing a 94.6% probability that the Fed will implement another 25 bps cut in October and an 87.4% probability of another one in December, which is more than the consensus two cuts that market in the year.

Can gold continue to climb? With bullion hitting numerous record highs this year and notching a staggering 50% YTD gain, investors are starting to get jittery, questioning if prices can continue to climb. While such concerns are understandable, gold continues to be well-positioned for further price appreciation. From a fundamental perspective, many of the tailwinds that contributed to gold's strong performance this year remain in play. Among these tailwinds are: i) US fiscal concerns; ii) Geopolitical and macroeconomic uncertainty; and iii) Central bank reserve diversification.

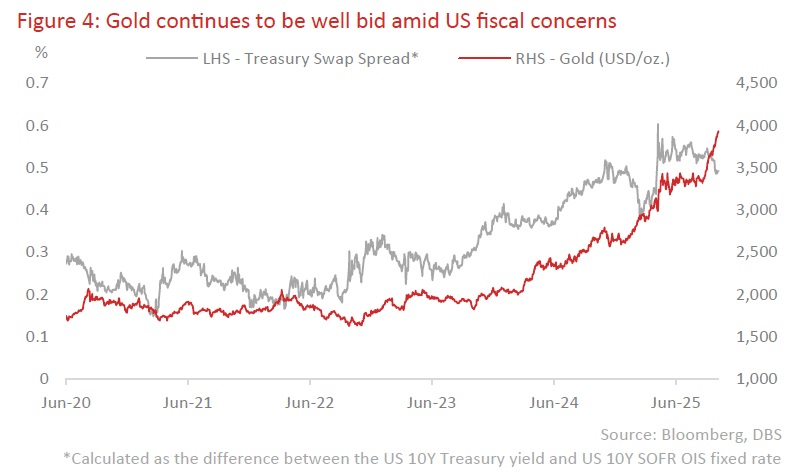

Fears of “fiscal dominance”. We have consistently highlighted that US fiscal concerns are only going to get worse given the expansionary nature of Trump’s One Big Beautiful Bill. This will exacerbate de-dollarisation and monetary debasement risks, which will in turn benefit hard assets such as gold. However, 3Q25 saw an escalation of such concerns into full blown fears of “fiscal dominance, a situation where the Fed is beholden to the government’s fiscal requirements rather than its mandate to maintain employment and price stability. With Trump’s attempted removal of Lisa Cook and subsequent inclusion of Stephen Miran in the Federal Reserve Board of Governors, market observers are raising red flags that central bank independence is coming under increasing threat. With Miran set to get a vote on the Federal Open Market Committee (FOMC), albeit only until next January, dissenting voices within the committee calling for loose monetary policy will now be stronger than ever. On a more conjectural level, Miran’s appointment suggests the hypothetical “Mar-a-Lago” accord may be closer to reality than once thought. After all, the tariff regime that he described in his paper titled “A User’s Guide to Restructuring the Global Trading System” is already being implemented. We have mentioned in past publications that any concrete steps to turn the Mar-a-Lago accords into reality will rapidly weaken the dollar, call into question the safe haven status of Treasuries, and ultimately benefit gold – this view remains relevant.

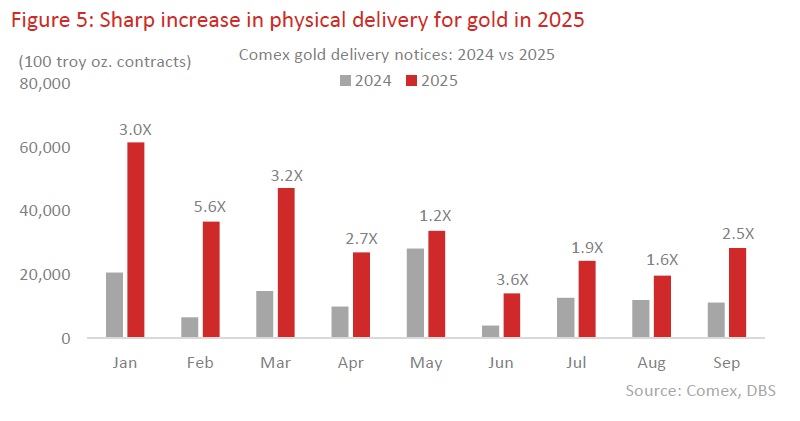

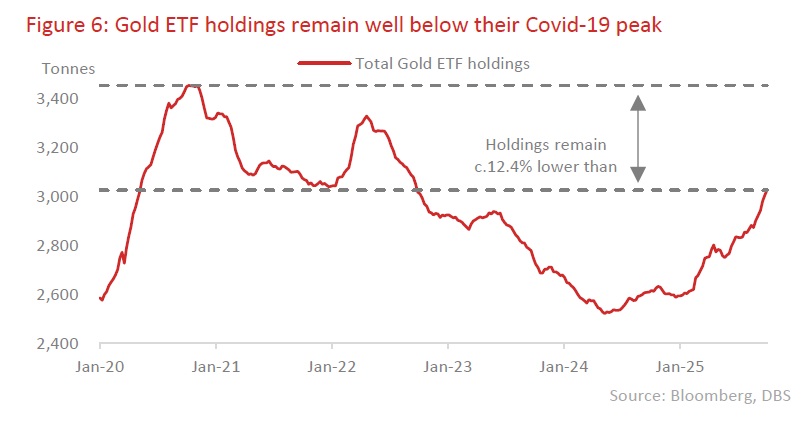

A safe haven amid heightened uncertainty. Another key driver of gold demand this year has been uncertainty; uncertainty around trade policy, geopolitics, and the inflation-growth dynamic to name a few. And this uncertainty has led to a significant uptick in investment demand for gold. On the physical gold front, 1H25 was the strongest first half for gold bar and coin demand since 2013. Two of the largest physical gold markets, China and India, saw a 44% and 7% y/y increase respectively in bar and coin demand in 2Q25. Comex gold delivery notices, which are official notifications from sellers in a gold futures contract on the New York commodities exchange that they are ready for physical delivery (as opposed to cash settlement), have also risen significantly in 2025, indicating a growing interest in physical gold as an uncertainty hedge. On the ETF front, flows have picked up substantially and consistently over the course of the year. However, total gold ETF holdings remain c.12% below their Nov 2020 peak, leaving plenty of headroom for further inflows. All in all, investment demand for gold will likely remain robust against a backdrop of persistent geopolitical and macroeconomic uncertainty.

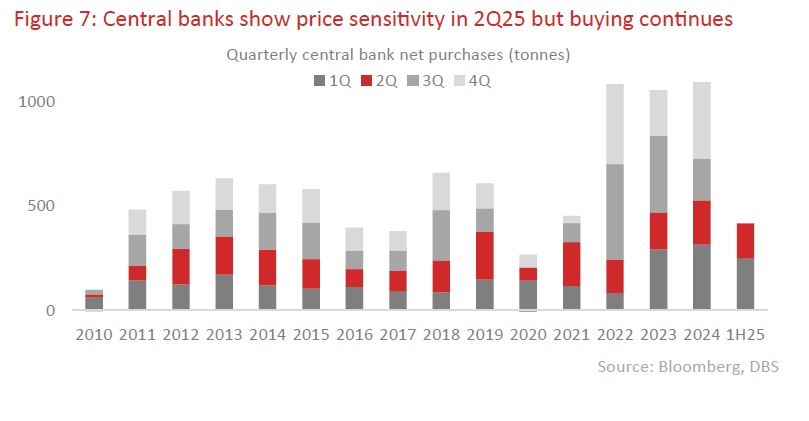

Central banks biding their time - buying intention remains robust. Since the Russia-Ukraine conflict of 2022, central banks have been accumulating gold as a means of reserve diversification; the financial sanctions that were subsequently imposed on Russia highlighted the risks of holding dollar-denominated assets and sparked a movement among central banks to diversify their foreign exchange reserves and hold a larger proportion of it in gold. As a result, we saw three consecutive years (2022 – 2024) of central bank gold buying exceed 1,000 tonnes, more than double the average between 2010 and 2021. Today, this sentiment remains as the Trump administration's ongoing efforts to impose a new world order, be it in trade or geopolitics, have only resulted in further global fragmentation.

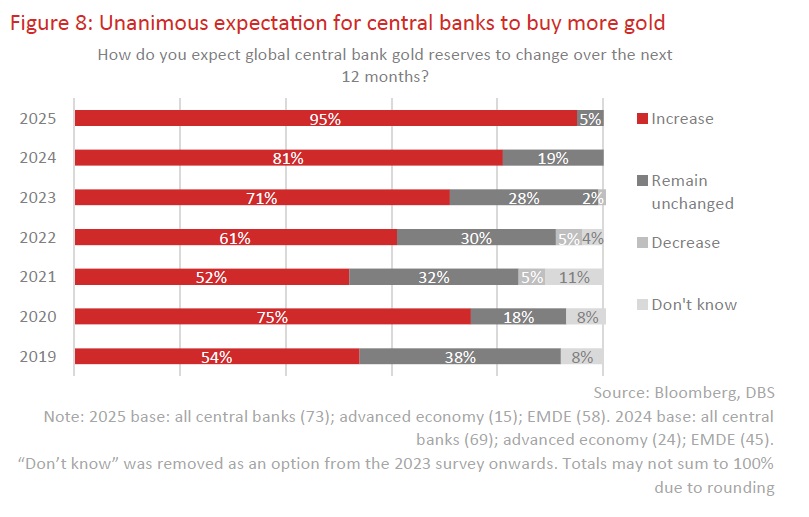

While 2Q25 saw central bank gold demand fall 33% q/q, buying for the quarter remains positive at 166 tonnes of net demand. The key thing to note is that this slowdown in buying does not mean that central banks are losing interest in gold. The likely cause of this moderation is the sharp increase in gold prices. Central banks are strategic buyers and often have target allocations to hit, however, that does not mean they are completely price insensitive; they can choose to slow their buying in response to record prices. Results from the 2025 central bank survey by the World Gold Council supports our hypothesis that central banks are still strongly in favour of increasing gold allocations, with a record 95% of respondents believing that official global gold reserves will increase over the next 12 months, and 43% believing that their own gold reserves will also increase during the same period.

Upgrade TP to USD4,450 by 1H26. Structural tailwinds for gold remain firmly in place, from fears of US fiscal dominance, to heightened geopolitical and macroeconomic uncertainty, and continued impetus for central bank reserve diversification. On a more immediate basis, we are seeing a revival of rate cuts as a positive catalyst for gold as labour market weakness in the US is fuelling wider growth fears. We are therefore upgrading our 1H26 target price from USD4,000/oz. to USD4,450/oz. on the assumption of a dollar index level of 92.9 and US 10Y Treasury yield of 4.2% by 1H26.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.