- FOMC cut the Fed Fund rate by 25 bps at September meeting; two more cuts are expected this year

- But stark inconsistencies are evident when one compares the economic projections with Fedspeak

- The mere act of cutting rates while concurrently upgrading economic projections highlights the deep divisions within FOMC

- Fed’s monetary easing at a time when inflation is 2.9% and with no recession in sight leads to a bigger question: Is the 2% inflation target still viable?

- Historically, a Fed easing cycle usually preceded major recessions with the S&P 500 registering average declines of 3% in subsequent 12 months

Related insights

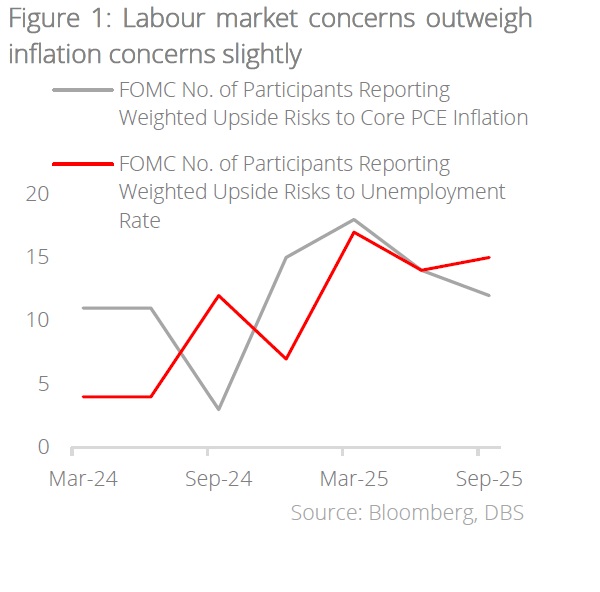

Labour vs Inflation Concerns: Sharp divisions in clear sight. The Federal Open Market Committee (FOMC) has, as expected, cut the Fed Fund rate by 25 bps at the September meeting. Based on the dot-plot, two more cuts are expected this year (up from one cut). Given the unprecedented political distractions surrounding the attempted ouster of Lisa Cook and appointment of Stephen Miran, the decision to cut by quarter basis point (as opposed to a larger cut) represents a victory for the embattled Fed Chair Powell, who in his press conference has made clear that inflation risks remain tilted to the upside and that policy is not on a preset course.

But stark inconsistencies are evident when one compares the economic projections with what Powell said in the news conference, for instance:

- Powell mentioned growing “downside risks to employment” in the press conference and yet, the GDP growth estimates for 2025 and 2026 have been revised up while the unemployment rate for 2026 and 2027 have been revised down.

- Economic projections are showing higher inflation risks for 2026 and yet, it is also forecasting more rate cuts ahead.

The mere act of cutting rates while concurrently upgrading economic and employment projections highlights the deep divisions amongst policymakers in the FOMC. This situation will likely get messier next year as potential changes in committee personnel takes hold.

Fed inflation target: Still viable? The Fed has a long-held inflation target of 2%. But with the central bank cutting rates now when: (a) core PCE inflation is at 2.9% and (b) there is no US recession in sight, the next natural thing to ask is: Does the Fed inflation target still matter? Indeed, given limited clarity on the full downstream impact of the tariff war and OBBBA, the Fed’s enthusiasm in cutting rates runs the risk of committing a major policy error further down the road. Perhaps, the Fed may have decided that labour market concerns supersede inflation concerns at this juncture. But as the central bank’s economic projections data shows, these concerns are separated by a fine line and the narrative will evolve in tandem with changes in incoming macro data.

Fed rate cuts in non-recessionary environment: Melt-up for risk assets. The start of a Fed rate cutting cycle has historically preceded major recessions. Since 1986, there have been four such instances. For example, the burst of the dot-com bubble saw the Fed cutting rates by 550 bps over a period of 30 months as a recession hit in Feb 2001. Thereafter, the Fed again cut rates aggressively during the subprime crisis as the economy fell into a downward spiral. During these occasions, the S&P 500 registered average declines of 3% in the subsequent 12 months.

There was, however, one occasion where Fed easing was not followed by a recession and this took place in 1995. After the initial rate cut, the S&P 500 registered gains of c.13.9% in the subsequent 12 months as the arrival of the Internet started a new industrial revolution and drove economic activities higher. Given strong AI-related capex in the current market, we believe that today’s environment mirrors that of 1995 and this augurs well for the resilience of risk assets.

Policy and macro uncertainties abound: Portfolio diversification is key. The trajectory of Fed policy will be highly dependent on incoming macro data and the potential impact from the tariff war remains a major wild card. Adopt a two-pronged approach in your portfolio construction: (a) ride the Fed policy easing wave with cyclicals like US Tech and EM assets like North Asia equities, and (b) hedge policy uncertainties with alternatives like gold, hedge funds, and private assets.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.