- Debt levels across DM is rising along with interest rates; concerns over US and Japan’s debt load have resulted in higher long to ultra-long yields

- Fed cuts expected, along with more buoyant EUR rates and a flattening JGB curve amid issuance tweaks

- Rate cuts expected across much of Asia, thanks to steady exchange rates

- CGB yields expected to stay steady after promising trade talks; an additional 20 bps cut in the 1Y LPR and a 50 bps reduction in the RRR are expected in 2H

- SGD rates are likely to maintain a sizable discount to USD rates with USD weakness being a more important driver

Related insights

Within the G3 space, bond vigilantes featured heavily since the start of the year. However, we should also consider the cyclical aspects as economic/political dynamics shift. Below we lay out our thought along these two themes:

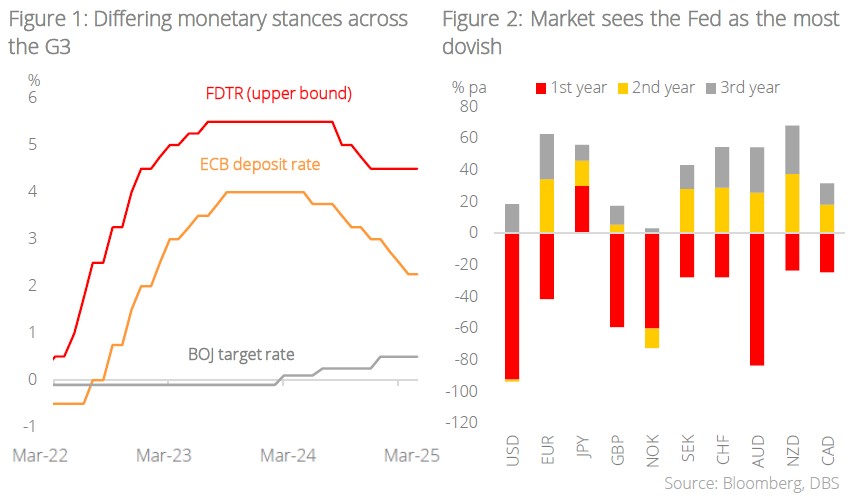

First, bond vigilantes have been on alert this year. Debt levels across the DM space is becoming elevated and historically, higher level interest rates (compared to the 2010s) are not helping. US’ spending on interest has now reached an annualised 3.2% of GDP as of Apr 2025. Within the G3, only Germany has a benign government debt load (60% of GDP). Worries about the US’ debt load (>100% of GDP) and Japan’s (>200% of GDP) have caused recurrents against the long to ultra-long end. Notably, 30Y US yields briefly poked above 5% and came within this cycle’s high of 5.17%. Meanwhile, there has been a relentless shift higher in ultra-long end JGB yields. Bund yields have been buoyant, but we think that investors are pricing in a more optimistic economic outlook rather than factoring in a higher required rate of return for fiscal laxness.

There are several watchpoints. In the US, the non-partisan CBO has indicated that Trump’s tariffs (if kept at current levels and without considering second order impact) could bring in USD2.8tn over the coming ten years, offsetting the extra USD2.4tn in spending that would come from extending the TCJA. This should perhaps ease some concerns on US debt at the margin but probably means that tariffs would have to remain at fairly high levels. It is not clear how much of Trump’s Big Beautiful Bill would pass. The public spat between Trump and Musk suggests vastly differing views at the administration. In the short term, at least, there is some hope that a compromise might be reached and the final bill that Trump gets to sign would be more restrained on the spending side. Monetary authorities/governments can also take some steps to cushion bond market volatility, including increasing bond buybacks (the Fed did it) or rejigging issuances away from the longer tenors (the MOF is mulling this while the UK has already done it). However, these steps only provide temporary relief. Investors need to regain confidence that DMs have their budget under control.

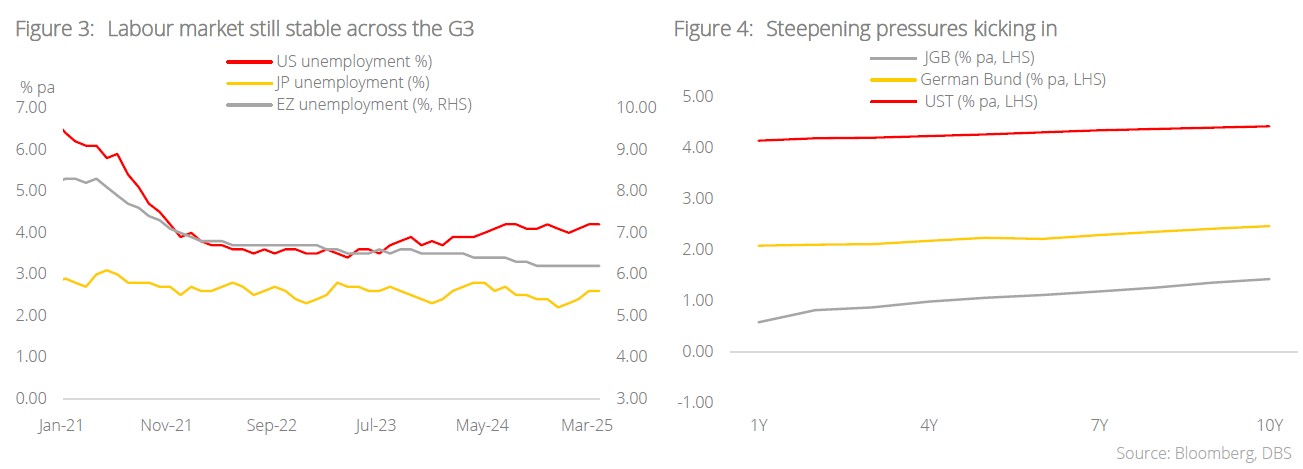

Second, economic dynamics are shifting. The growth outlook is generally challenging across the DM amid the trade war. Despite the resilience of NFP, we think that doubts about the US economy’s strength would remain. A stronger case could be made for further calibrated cuts with US inflation surprisingly well behaved thus far. Bets on rate cuts would probably keep a bid on front-end USTs. Meanwhile, the ECB has been steadily cutting rates, but with the policy rate already at 2% (at neutral), Lagarde has indicated that there may not be much room to ease further. In any case, if the tariff war stays as-is and fiscal spending kicks back in, the outlook for the Eurozone may turn more positive. Lastly, the BOJ is still facing considerable inflation pressures and is therefore incentivised to further normalise policy settings. However, the volatility of the yen and gyrations in the ultra-long tenors means a quicker rate hike path is difficult.

The upshot is that the Fed and ECB are likely to shift gears. After the extended pause, we see the Fed cutting 50 bps in 2H with the market likely to demand more in 2026. The ECB may be close to done (if not already done) for the time being. Meanwhile, the BOJ remains on the slow tightening path. We see a decent chance that US yields would shift lower in the coming few months as market participants mull a US economic slowdown, further steepening the curve in the process. Meanwhile, we think EUR rates would be somewhat more buoyant. Lastly, the JGB curve may be due for some flattening pressures amid ongoing BOJ tightening and a potential tilt in issuances away from the long end, into the short tenors.

Asia Rates

CNY rates: Limited upside in CGB yields

The onshore CGB yields are expected to stay steady after the promising trade talks. While recent data print surprised on the upside, investors are not comfortable with the cloudy growth outlook. First, exports growth could ease after the 90-day truce. Contracting imports reflect softer demand for intermediate goods as manufacturers brace for weaker orders. Second, subdued investment sentiment is evidenced by the sharp divergence between robust government bond issuance and soft private credit growth. Household sentiment is also under pressure from weak job prospects, declining income growth, and the negative wealth effect from the property market. Third, the deterioration in credit demand can be partly attributed to elevated real interest rates. Tariff driven overcapacity and frontloading will weigh on producer prices. For instance, we note a diverging trend between rising automobile production and investment vs tepid domestic sales and exports. Auto PPI thus underperforms the already deflating headline PPI.

Further easing is warranted. After the recent cuts, we expect an additional 20 bps cut in the 1Y LPR and a 50 bps reduction in the RRR in 2H. These could keep CGB yields in check. More importantly, incremental liquidity could flow into the fixed income market in the midst of weak credit demand. The share of bond investment within financial institutions’ portfolio stays with its march. China’s bond market also received the strongest inflow amongst Asia EM peers since the Two Sessions in March, especially after the announcement of the rate cut on 7 May.

IDR rates: Rate cut and fiscal developments

IndoGB yields are expected to fall moderately. Domestically, easing growth momentum (we have downgraded our growth forecast to 4.8% this year, compared to 5% previously) and contained CPI calls for further monetary easing. While this was constrained previously, USD weakness should allow for another 50 bps cut in 2H25. Liquidity conditions have also become much more flush with recent SRBI auctions showing low rates despite an increase in auction sizes. While fiscal slippage is a concern keeping the curve steep, we suspect that investors would be willing to reach for yield in this environment. IndoGB yield differential against USTs will also likely compress further.

INR rates: Compressing IGB-UST spreads

Demand for India bonds has been recovering steadily since the third week after the US’ “Liberation Day.” Equity markets have also seen net foreign inflows. India’s favorable fiscal position, easing inflation, a lower terminal repo rate, and inflows from the “China+1 Strategy” are the key catalysts. On the fiscal front, the February budget set a central government deficit estimate of 4.8% and 4.4% of GDP for FY25 and FY26, respectively. RBI’s dividend transfer further supports IGBs, providing a cushion of +0.12% of GDP to the fiscal deficit.

Against this backdrop, liquidity conditions appear to be easing. The RBI has injected net INR5tn YTD, and cut the benchmarked rate by 50 bps surprisingly earlier on 13 Jun. The spread between overnight MIBOR and the policy repo rate has fallen below zero. Finally, still-elevated US tariffs on Chinese imports are inducing FDI inflows.

Strategy-wise, a further grind lower in short end yields may be possible under benign global conditions. However, the largest part of the adjustment may be largely done as further RBI easing requires weak data. Second, we think that there may be interest to extend duration out to 10Y segment. The yield pickup would likely prove enticing to investors in a weak USD environment.

KRW rates: Rate cuts and ongoing fiscal spending

The KTB curve steepened on the back of monetary easing and expectations of increased long-end KTB supply post elections. The supplementary budget plan, along with potential welfare spending under the new government, points to a much more aggressive fiscal stance as political uncertainties/gridlock gets put behind. That said, the selloff in KTB is orderly as market participants are not overly concerned about the debt load. Instead there is arguably more optimism about Korea, especially when we look at the performance of the won. We think that investor interest will return to the long end after the recent yield adjustment.

MYR rates: Outperforming MGS as door for first cut opens

A prospective easing cycle by BNM should support long MGS positions. Asia central banks are already on course with rate cuts since 2024, and BNM has just opened the door for looser monetary policy. Despite holding its OPR at 3.00% on 8 May, BNM provided a more downbeat economic growth outlook, alongside slashing the statutory reserve requirement ratio by 100 bps, which will inject c.MYR19bn worth of liquidity into the banking system. Rising global risks from escalating trade tensions are negative for Malaysia’s export-oriented sectors and the economy is set to miss its current official 2025 growth projection of 4.5-5.5%. Steepening will at play as investors bet on the start of the rate cut cycle.

PHP rates: Reaching terminal rate in 3Q25

The BSP is on course with its rate cuts. Another 50 bps cut is likely, bringing the benchmark overnight repo rate to its terminal level of 5.00% by the end of 3Q25. Including the previous 100 bps in cuts, the BSP will have reduced the policy rate by a total of 200 bps since mid-2024. While previous reciprocal tariffs on the Philippines were relatively low at 17%, a potential trade war renewal poses risks to the external sector. The US accounted for over 15% of the country’s exports in 2024. Potential spillover effects on the domestic economy and labour market warrant concern. On the monetary front, rapidly decelerating CPI inflation, which fell from 8.7% in early 2023 to 1.4% in Apr 2025, allows further rate cuts. At this juncture, the real interest rate remains restrictive at 4.1%. Short-end Philippine government bond yields will see more notable downward pressure, and the spread against UST yields should compress.

SGD Rates: Widening discount vs USD rates

The discount of SGD rates vs USD rates has been widening since the start of the year. In the front of the curve, SORA fixings have been grinding lower even as the Fed stayed on hold and the MAS flattened the SGD NEER slope. At the start of the year, it was flush SGD liquidity that drove SGD rates lower. This was exacerbated over the past two months as confidence in USD assets eroded amid the tariff war and large US fiscal deficits. In the rates space, it meant that a premium had to be built into USD interest rates. Simultaneously, there are more flows into SGD assets as investors rebalance away from the USD. Accordingly, SGD rates are likely to maintain a sizable discount to USD rates with USD weakness being a more important driver for relative value than the slope of the SGD NEER.

THB rates: Growth downgrade

We see further downside risks to THB rates. The BOT has the potential to cut its policy rate by another 75 bps over the next 12 months, following the two 25 bps reduction in 1Q-2Q25. Despite narrowing monetary policy space, this easing trajectory is relatively aggressive compared to other Asian central banks due to underperforming growth. Economic growth will likely slow amid external uncertainty. Thailand's share of goods exports to the US has increased since Trump's first term, the Covid pandemic, and into his second term. Tourist arrivals have weakened as Thailand loses market share to other regional destinations. Domestically, consumer confidence is softening due to economic uncertainty and job security concerns. We have lowered our 2025 GDP growth forecast to 1.8%, easing from 2.5% in 2024. Headline inflation that is below the BOT’s 1-3% target also creates room for rate cuts. Strategy-wise, Thai government bond yields will likely fall further, with a steepening yield curve as the core theme.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.