You are in Wealth Management

ATM & Branch

Help & Support

Why Us

Invest

Insure

Banking

Accounts

Credit Cards

Borrow

Wealth Planning

Research

ATM & Branch

You are in Wealth Management

Personal Banking

DBS

Wealth Management

DBS Treasures

DBS Treasures Private Client

DBS Private Bank

DBS Vickers Securities

DBS Vickers Online

Business Banking

SME Banking

Corporate Banking

DBS Group

About DBS

Why Us

Invest

Insure

Banking

Research

Created with Sketch.

Login

Popular Search

Credit Cards,

Promotions,

ATM & Machines,

iBanking,

Home Loans,

Myself

Accounts

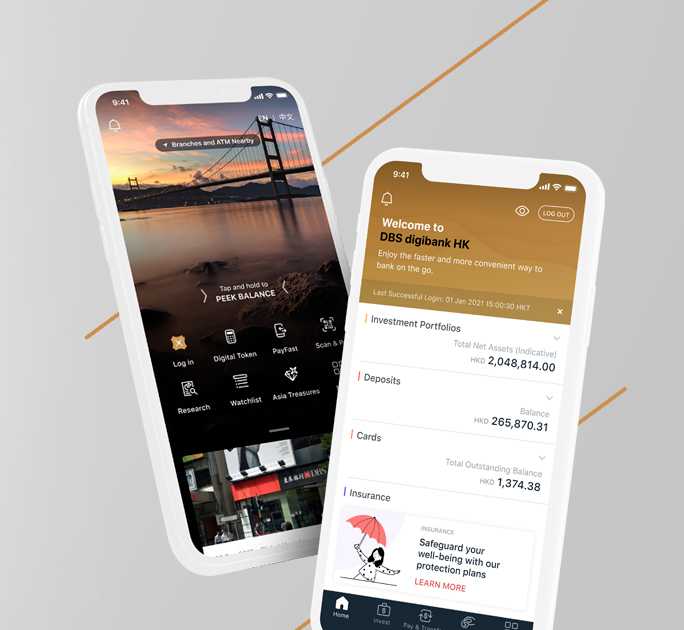

DBS digibank HK app

More intuitive than ever

Learn More

Leverage your Investment

Learn More

Trading with our Platform

Learn More

Featured

Product Suite

Wealth Management Account

Investments

DBS digibank HK

Equity Funds

Trading with our Equity Specialists

Currency Linked Investments

Investment Grade Bonds

Useful Links

Latest Investments Offers

Exchange Rate

Investment Objective Setting

Important Documents

Investment Products Consolidated Terms & Conditions

Disclaimer

Market Update and Tools

Market Focus

New Fund Spotlight

Fund Analytical Tools

Talk to our Staff

(852) 3668 8008

Or let us

contact you

Other hotlines

Others

Feedback Form

Video training on General Knowledge of Derivatives

IPO Shares Subscription Service

IPO Allotment Result

Need help?

Ways to get our

Help & Support

Markets

Hong Kong

EN

繁

Mainland China

India

Indonesia

Singapore

Taiwan

Hong Kong

EN

繁

Web Conditions of Use

Data Policy

Vulnerability Disclosure Policy

©Copyright. DBS Bank (Hong Kong) Limited 星展銀行 (香港) 有限公司